Informal employment: fiscal implications for municipalities (assessment of revenue losses and growth potential)

Background

In 2024, a study titled “Modelling the Impact of Changes in the Personal Income Tax Allocation Mechanism on Municipal Budgets” was conducted at the request of U-LEAD with Europe.[1] The study demonstrated that a transition to allocating PIT to the budgets of municipalities based on the taxpayer’s place of residence would lead to increased revenues for most small and medium-sized municipalities, a significant number of whose residents work outside their jurisdiction. Conversely, such a change may pose risks to the financial sustainability of municipalities that currently benefit from substantial revenues due to the concentration of employers within their territories. In this context, the search for additional sources to strengthen the financial capacity of municipalities is of particular importance.

One such factor is the decline in informal employment and the concomitant increase in formal economic activity. Informal employment directly affects the socio-economic development of municipalities, the functioning of local labour markets, competitive conditions and the formation of the revenue base of local budgets, primarily resulting in shortfalls in PIT and single tax revenues. Developing effective policy in this area is hampered by the fact that, following the onset of the full-scale war, the regular collection of statistical data on informal employment has been suspended, and no systematic assessment at the local level had previously been conducted.

Given the lack of official data, U-LEAD with Europe experts carried out an assessment of the level and structure of informal employment, the volume of foregone revenues from PIT and single tax attributable to informal employment, as well as the potential for their increase. This assessment was based on data from a representative sample survey of residents of municipalities. The full report is available at the following link.

Impact of the Full-Scale War on Informal Employment

According to the survey of residents of municipalities, the level of informal employment increased from 19.3% in 2021[2] to approximately 26.2% in 2024. This figure is likely somewhat higher than the annual average, as the survey was conducted in August–September, the period of peak seasonal employment.

The structure of informal employment has also changed. During 2015–2021, there was a downward trend in the number of informally employed persons within registered enterprises, driven by strengthened state policies aimed at reducing informality. Currently, the reverse trend is observed: the share of informally employed individuals within registered enterprises has increased from 37% to nearly 45% of total informal employment. Such changes may be associated with the suspension of state supervision (control) measures under martial law. Another contributing factor may be the use of informal employment as a means of avoiding military registration requirements.

Traditionally, the highest level of informal employment remains in agriculture, forestry and fisheries, exceeding 60%. A notable increase has also been observed in the construction sector, where the rate has reached 57%. While in the pre-war period this indicator showed a steady downward trend, it has now approached its peak level recorded in 2015.

The most significant increase in informal employment has been observed in large urban municipalities that have become hubs for internally displaced persons. At the same time, these municipalities face a substantial shortage of qualified labour, particularly in construction and transport, where this deficit is partially offset by the engagement of informally employed workers.

Assessment of Budget Revenue Losses Due to Informal Employment

Budget revenue losses attributable to informal employment are defined as the amount of tax revenues that could have been collected if informal employment was fully formalised. According to estimates, in 2024 such losses exceeded UAH 76.4 billion, of which UAH 67.5 billion is attributable to foregone PIT revenues and UAH 8.9 billion — to single tax. In relation to actual revenues, these losses account for 3.8% of total tax revenues of the general fund of the consolidated budget of Ukraine, 21.0% of PIT revenues derived from wages and 16.1% of single tax revenues.

The largest losses are borne by the budgets of municipalities, which account for 66% of the total losses, or more than UAH 50.4 billion (see Figure 1). For comparison, this amount represents approximately 13% of the actual tax revenues of their budgets.

Figure 1. Structure of Losses from Informal Employment by Budget Level

Potential for Growth in Budget Revenues Through Formalisation of Informal Employment

The potential for growth in budget revenues reflects the expected increase in PIT and single tax revenues that may be achieved through a reduction in informal employment as a result of implementing relevant policy measures. The estimates are based on a differentiated approach that takes into account the socio-economic nature of various forms of informal employment, regulatory practices applied in EU countries, and the current institutional environment in Ukraine.

The calculations do not assume the complete eradication of informal employment. It is important to note that certain forms of informal employment have limited fiscal impact. Furthermore, the costs of their formalisation may exceed the expected benefits, or lead to adverse social consequences. In particular, self-employment within personal subsidiary farming in many small, especially remote municipalities, primarily serves an adaptive function and is not considered a realistic source of increased budget revenues in the medium term. By contrast, informal employment within the formal sector is significantly more responsive to regulatory intervention, and it is within this segment that formalisation may generate the greatest fiscal effect. This approach helps to avoid overestimation and focuses attention on areas where formalisation is both feasible and most effective.

According to scenario-based estimates, the potential increase in tax revenues ranges from UAH 19.5 billion to UAH 30.1 billion. The intermediate scenario, considered the most realistic for Ukraine, is presented below. Under this scenario, additional tax revenues could amount to UAH 25.9 billion, or 34% of the total losses attributable to informal employment, including: UAH 24.6 billion from personal income tax (36%); UAH 1.2 billion from single tax (14%).

Of this amount:

- UAH 6.2 billion would accrue to the state budget

- UAH 3.3 billion to regional budgets

- UAH 16.4 billion to the budgets of municipalities.

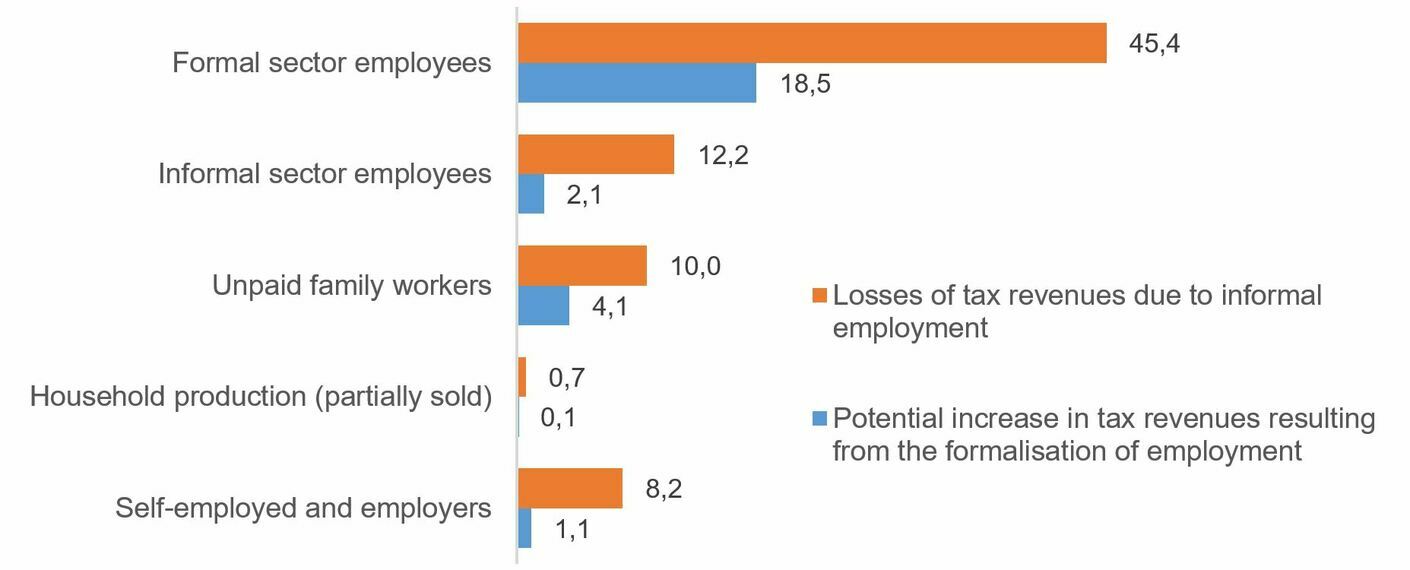

The greatest opportunities for formalising employment relationships are associated with informally employed wage workers in enterprises operating within the formal sector. The formalisation potential for this group is estimated at approximately 40%. At the same time, this indicator varies significantly depending on enterprise size and type of economic activity: at enterprises employing more than 50 persons, it exceeds 70%; at small enterprises with fewer than 5 employees, it is below 20%. Overall, this segment of informal employment could generate approximately UAH 18.5 billion in additional tax revenues (see Figure 2).

Figure 2. Potential Increase in Tax Revenues by Categories of Informally Employed Persons, UAH billion

If the transition to allocating PIT based on the taxpayer’s place of residence ensures a more equitable distribution of resources and reduces disparities in fiscal capacity among municipalities, then employment formalisation policy may serve as an additional compensatory instrument for municipalities that incur losses as a result of such a change. Accordingly, further analysis of differences between types of municipalities in terms of budget revenue losses from informal employment, as well as the assessment of their growth potential, is conducted under the assumption that PIT is allocated to the budgets of municipalities based on the taxpayer’s place of residence.

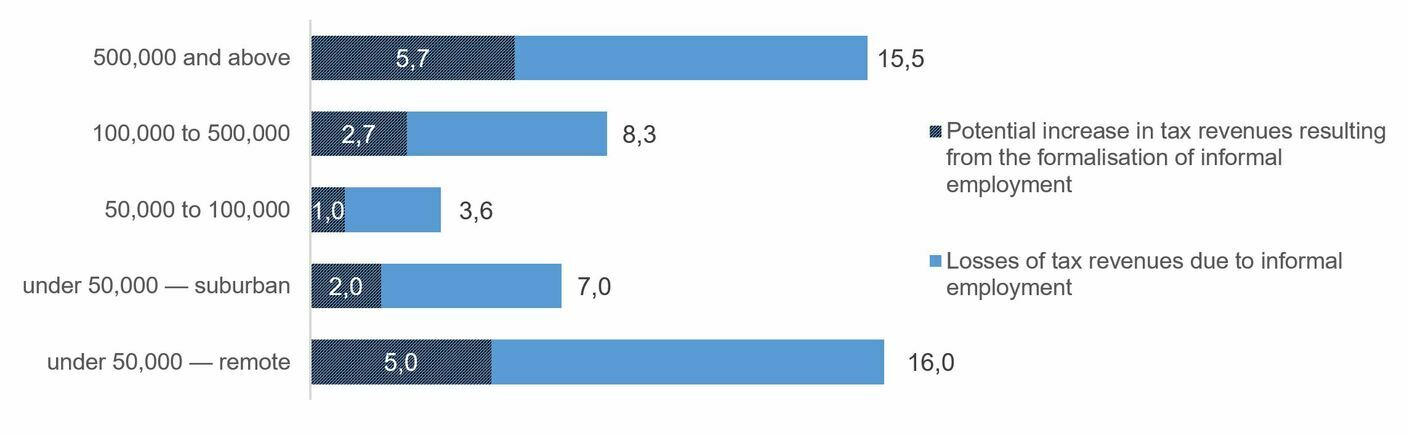

Although the level of informal employment is higher in small municipalities with populations below 50,000, the largest increases in tax revenues from formalisation are expected in large cities (see Figure 3). This is due to the concentration of a significant number of informally employed wage workers with wages above the national average. By contrast, in small, particularly remote municipalities, a considerable share of informal employment consists of individuals engaged in self-employment within their own households, who sell part of their output on the market. However, the financial losses associated with this category remain relatively small due to two key factors. Firstly, the relatively low income levels and, secondly, the predominantly seasonal nature of such activities.

Tax revenues to the budgets may also increase significantly through the reduction of various forms of so-called undeclared work. The concept of undeclared work is widely used in EU countries and, in addition to informal employment, encompasses other forms of concealed economic activity, including the payment of “envelope wages” and the use of various legal arrangements — such as bogus self-employment, internship agreements, or outsourcing contracts — to disguise de facto employment relationships.

Figure 3. Potential Increase in Tax Revenues to the Budgets of Municipalities, UAH billion

In Ukraine, bogus self-employment, where a worker is formally registered as a sole proprietor but is in fact engaged in an employment relationship, is frequently used by employers to reduce tax and social contribution liabilities and to avoid compliance with labour law requirements. Taking into account that losses in PIT revenues are partially offset by the payment of the single tax, the net fiscal losses resulting from the prevalence of bogus self-employment are estimated at approximately UAH 7.4 billion, including UAH 3.2 billion attributable to the state budget, UAH 0.9 billion to regional budgets and UAH 3.3 billion to the budgets of municipalities. These estimates are indicative, as some respondents may not have fully understood the legal nature of their employment relationships or may have provided incomplete information regarding the terms and level of remuneration.

Recommendations

A retrospective analysis demonstrates that the level of informal employment can be significantly reduced through the implementation of consistent and effective public policy. During 2015–2021, amid intensified government measures, including enhanced labour inspections, the level of informal employment declined from 26.2% to 19.3%. International comparisons indicate that the potential for further reduction in Ukraine remains substantial.

The opportunities for employment formalisation and the timeframes for its implementation largely depend on the effectiveness of public policy, which should be differentiated and combine enforcement measures with instruments to support entrepreneurship and expand opportunities for formal employment. Local self-government bodies should play a key role in implementing such policies, given their proximity to local economies and their deeper understanding of local labour market dynamics. This requires the development of systematic cooperation between local self-government bodies, the State Labour Service, tax authorities and other public institutions. In this context, it is recommended to:

- introduce procedures for regular information exchange between the State Labour Service and local self-government bodies and, in the longer term, establish an information and analytical system for monitoring the financial and socio-economic development of municipalities based on data from state registers and other sources

- define in regulatory instruments the procedures for interaction between the State Labour Service and local self-government bodies, including procedures for submitting information on potential violations of labour legislation, timelines for its review, response mechanisms, and reporting on outcomes

- consider introducing financial incentives for local self-government bodies to participate in combating informal employment, in particular by allocating a portion of fines for violations of labour legislation to local budgets. The experience of 2019–2021 indicates that such an approach increased the engagement of local self-government bodies in identifying informal employment

- establish permanent coordination mechanisms between the State Labour Service, tax authorities, local self-government bodies, the employment service, and other relevant stakeholders.

Another key area of focus is the integration of mechanisms to prevent informal employment into post-war recovery planning. In view of the considerable demand for labour and the extensive use of budgetary and donor funding, it is recommended that specific requirements be established for contractors implementing reconstruction projects. Evidence from international best practice shows that effective prevention of informal employment is achieved through a combination of qualification requirements for tender participants, verification of workforce capacity, regular reporting on labour engagement and monitoring compliance with applicable legislation during contract execution. It is recommended to:

- include in tender documentation and contracts a requirement to engage only formally employed workers for activities that, by their nature, constitute employment relationships. Similar approaches are applied in EU countries in accordance with Directive 2014/24/EU of the European Parliament and of the Council of 26 February 2014 on public procurement

- strengthen requirements for confirming the workforce capacity of tender participants, including the number of employees, key personnel, workforce engagement plans, and subcontractors

- introduce regular contractor reporting on workforce utilisation throughout the period of contract performance

- ensure systematic monitoring of contractors’ compliance with labour law requirements concerning employment relationships and working conditions throughout the entire contract performance period[3].

[1]Modelling the Impact of Changes in the Personal Income Tax Allocation Mechanism on Municipal Budgets, U-LEAD with Europe, 2024.

[2]Data from the State Statistics Service of Ukraine based on the Labour Force Survey (LFS).

[3]An example of such an approach is the DURC system in Italy, which provides for regular verification of contractors’ compliance with employment and social contribution obligations in the course of public contract performance.

")

Attached files:

Source:

U-LEAD з Європою

25 July 2026

Майбутнє українських громад: Олександр Корнієнко - у подкасті «Врядування»

Майбутнє українських громад: Олександр...

«Якщо хоча б третина наших громад зможе одним реченням сказати, що це за громада і чого вона хоче,...

24 July 2026

Реорганізація чи перепрофілювання: як не помилитися, створюючи ліцей

Реорганізація чи перепрофілювання: як не...

Сесія ради громади відбулася. Рішення ухвалено. Школа І–ІІІ ступенів має стати академічним ліцеєм і,...

24 July 2026

Not Just for Diplomats: Seven Principles of the...

International engagement by Ukrainian communities has changed dramatically in recent years Whereas it was once...

23 July 2026

Is it really enough simply to identify several...

This process actually requires a much more in-depth analysis: primarily, of the number of future senior school...